In a great article written by Tax Pro Connections today we get the highlight of the details of the bill that was passed on December 18. It outlines some extenders but also a lot of rules that have now been made permanent. One of them leading to 100% tax-free income. One of my favorite types 🙂 below you can see the awesome article written by tax Pro connections. I note that it is this time of year in which it is super important to have a plan before the end of the year is up. What would you do with 100% tax-free income?

Obama Signs Extenders Bill

Some Extended Through ’16, ’19; Some Permanent

by Jon A. Hayes,

Tax Preparer Conections

December 21, 2015 — The Protecting Americans from Tax Hikes Act of 2015 (PATH) was signed into law by President Obama on December 18, 2015. It includes numerous extensions of many tax provisions with various lengths. Some of the changes are permanent, while others extend for one to three years. Here is a synopsis of those changes:Individuals

Permanent Extensions

- The $250 deduction for educator expenses. The amount now adjusts for inflation.

- The state and local sales tax deduction.

- Qualified charitable distribution (QCD) from an IRA of up to $100,000 per year.

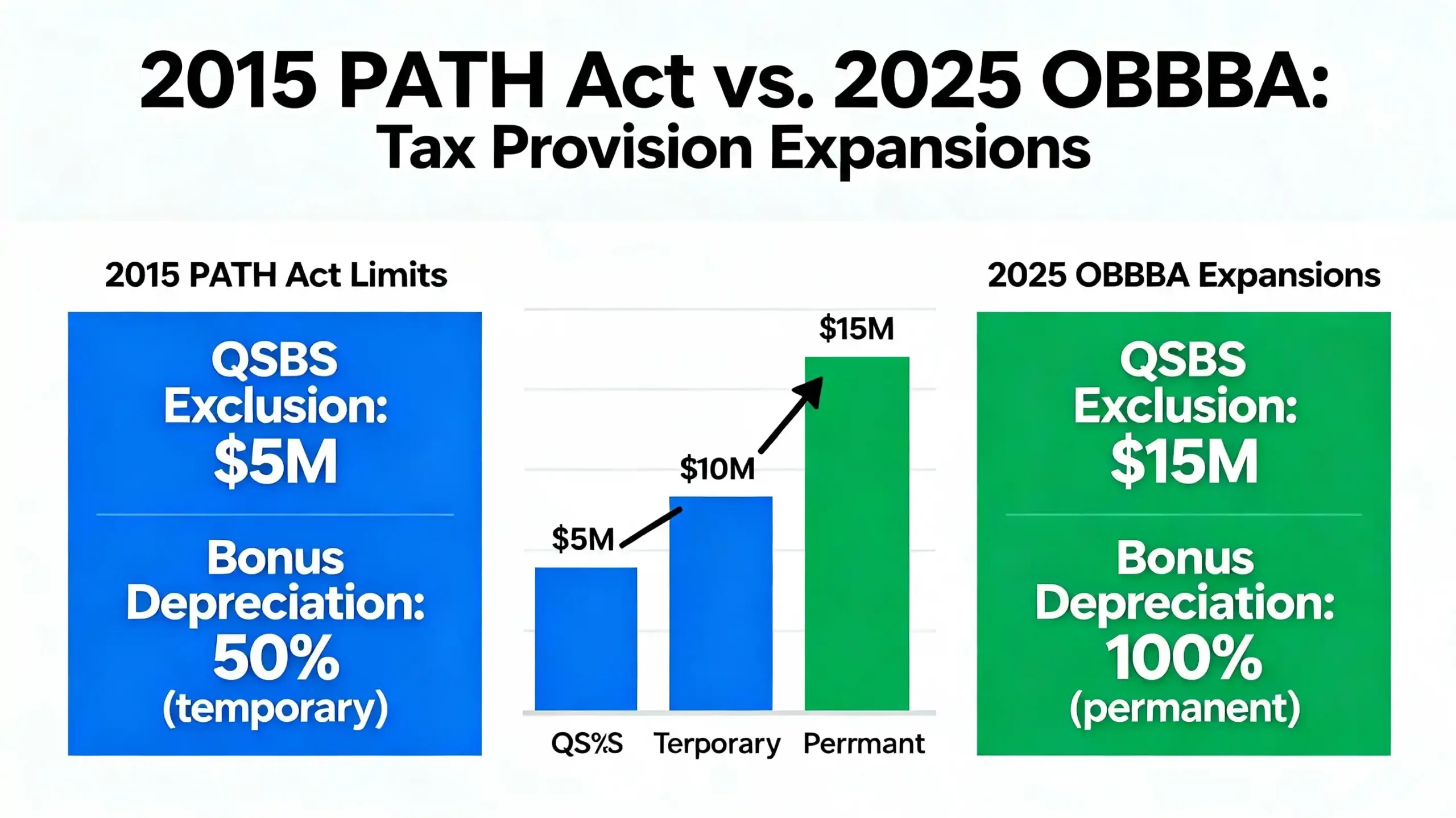

- The 100% §1202 exclusion on qualified small business stock.

- Earned Income Credit. The EIC “marriage penalty” relief and credit increase for those with three or more children. Taxpayers are no longer allowed to claim EIC for years in which a social security number was not obtained by the due date of the tax return.

- The American Opportunity Tax Credit. Taxpayers are no longer allowed to claim the American opportunity tax credit for years in which a taxpayer identification number was not obtained by the due date of the tax return. Institutions are now required to report the amount paid for education expenses for years beginning after 2015. Claims for the American opportunity tax credit requires an EIN from the institution.

- Child Tax Credit. Instead of increasing the threshold for the additional child tax credit to $10,000, The Act keeps the threshold at $3,000 permanently. Taxpayers are no longer allowed to claim the child tax credit for years in which a taxpayer identification number was not obtained by the due date of the tax return.

- Section 529 plans now allow expenditures for computers, peripheral equipment and Software provided they are to be used primarily by the beneficiary during years of academic study.

- Under the Act, the $500 penalty for failure to comply with EIC due diligence is now expanded to include the child tax credit and American opportunity tax credit.

Extensions Through 2016

- Cancellation of debt income exclusion on qualified principal residences.

- Mortgage insurance premiums paid or accrued allowed as a deduction.

- The tuition and fees deduction.

- The credit for nonbusiness energy placed in service, such as windows, doors, etc. The residential energy efficiency credit (REEP) under §25D is still set to expire at the end of 2016.

- 10% credit for purchases of electric powered 2-wheeled vehicles is extended, such as electric motorcycles. The Act did not extend the credit for 3-wheeled vehicles.

Businesses

Permanent Extensions

- §179 $500,000 limit increased to $500,000. In addition, expensing “off-the-shelf” software is also made permanent. The restriction

on heating and air conditioning units has been eliminated. - The 15-year life is made permanent for the following qualifying properties: qualified leasehold improvements; qualified restaurant buildings, and qualified retail improvements.

- The 5-year recognition period for built-in gains of an S corporation that was previously a C Corporation.

- The Credit for Increasing Research Activities (the research credit). Eligible small businesses can claim the credit against AMT. Eligible small startup companies may offset their FICA tax liability with the research credit.

- The ability to limit the reduction in basis for charitable contributions made by an S corporation to the property’s adjusted basis.

- Transit passes and van pool benefits.

- The due date for W-2s and W-3s and returns reporting nonemployee compensation have changed. The new due date is January 31 for tax years beginning after the enactment of the act. For most taxpayers, this is tax year 2016. Any information returned now has a de minimis safe harbor for errors. If an information return has an error of $100 or less ($25 or less for withholding), no correction is required.

Extensions Through 2016

- The clarification of a racehorse as three year property.

- Qualified film expensing. The Act contains a provision to include live theatrical performances.

- The alternative fuel vehicle refueling property credit.

Extensions Through 2019

- The 50% bonus depreciation applies to property placed in service through 2017, then reduces to 40% for 2018 and 30% for 2019.

- The act extends the first year depreciation for passenger automobiles subject to §280F limitations. The Act allows for the additional $8,000 of bonus depreciation through 2016, then $6,400 for 2018 and $4,800 for 2019.

- The Work Opportunity Tax Credit. The Act also includes a provision to allow a credit for qualified long-term unemployed individuals.